RIO is a free monthly publication that provides insights from our economists into what rail traffic says about today’s economy and where the data suggests it could be headed. As part of RIO, the Freight Rail Index (FRI) tracks movement across the most economically sensitive rail traffic commodities. You can find the full report each month on this webpage, with past editions available as PDFs at the bottom of the page. Find past edition PDFs at the bottom of this page.

July 2026 Key Takeaways

- Rail traffic continues to strengthen. Six consecutive months of carload growth point to sustained improvement in freight demand.

- Growth is becoming more broad-based. More commodity groups are participating in the expansion, suggesting freight activity is becoming healthier and more durable.

- Manufacturing and freight activity are becoming more aligned. Rising factory output and stronger shipments of key industrial commodities are reinforcing the same positive economic signal..

- The second half of 2026 is starting from a position of strength. Freight demand enters the second half with more momentum, broader participation, and stronger underlying fundamentals than it had at the start of the year.

Rail Traffic Signals a Broader Industrial Expansion

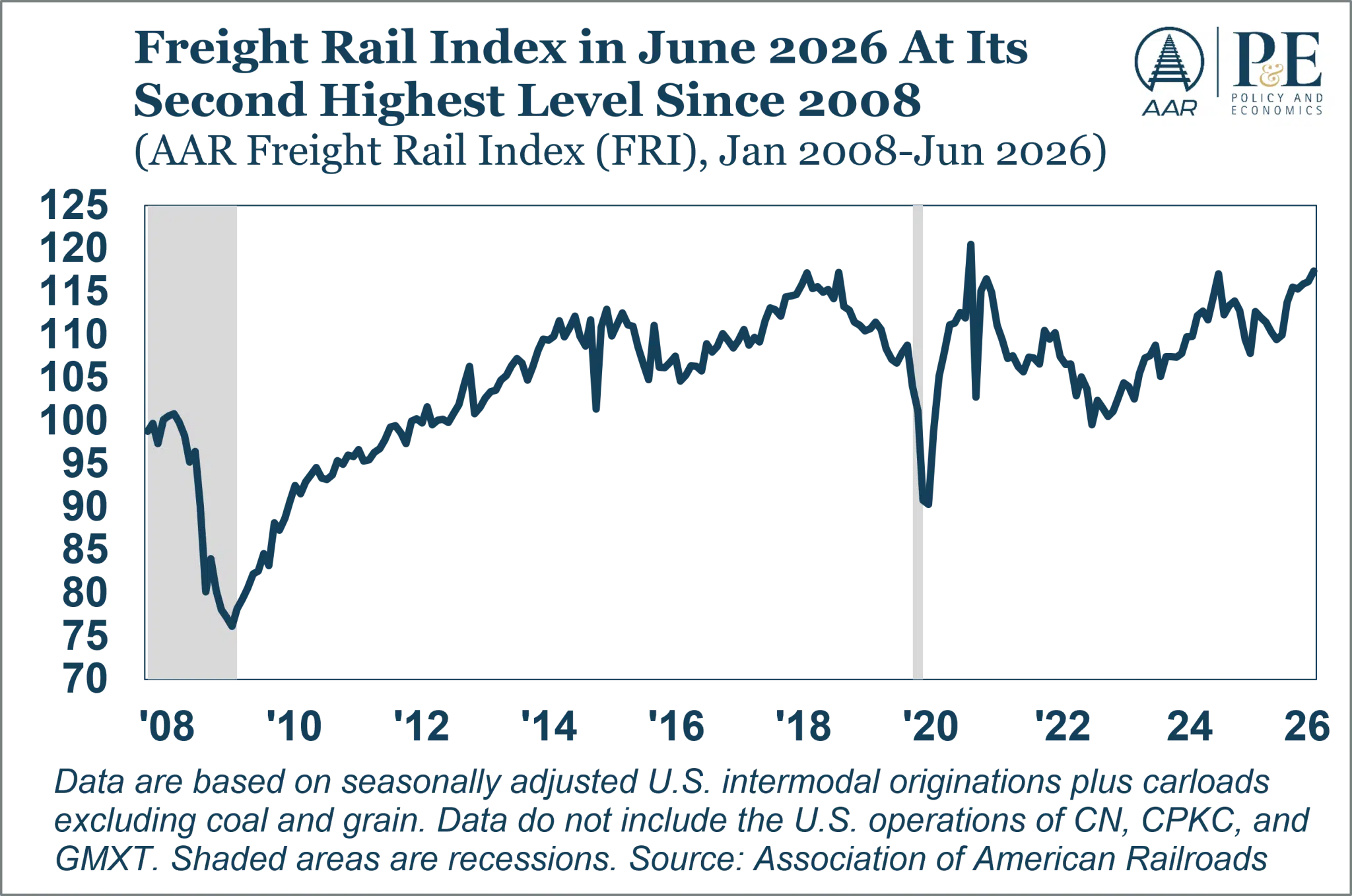

June extended a pattern that has been building throughout 2026. Weekly average intermodal volume reached a new monthly record, while average weekly carloads were the highest since May 2021. Total carloads rose from a year earlier for the sixth consecutive month and intermodal for the fifth.

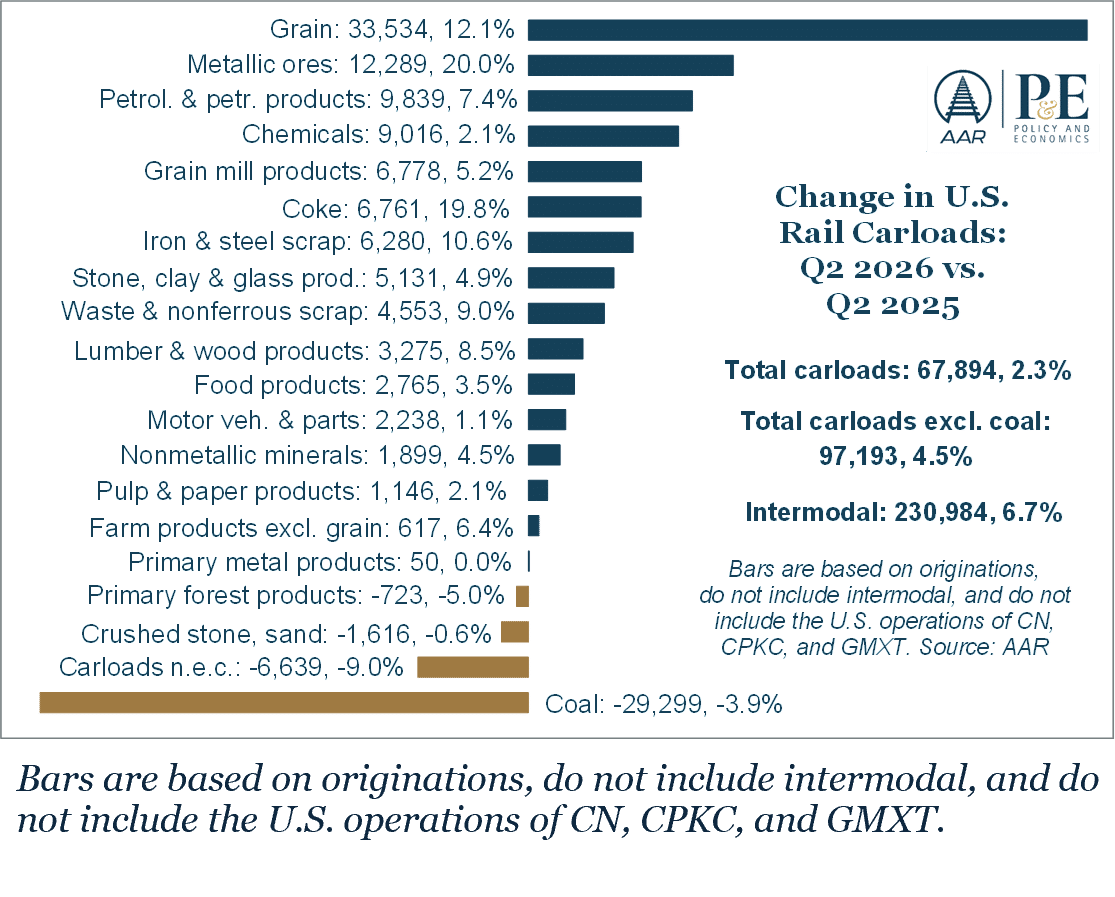

What stands out, however, is not simply that traffic is increasing, but that the gains are becoming increasingly broad-based across commodity groups. Fourteen of the twenty major carload categories posted year-over-year gains in June, and several reached year-to-date highs. Economists often focus on how fast something is growing. Equally important is how broad that growth is. When growth becomes more widespread across industries, economic expansions tend to be more durable.

Rail is not the economy, but it remains one of the clearest real time indicators of activity across the goods producing sector. While uncertainty around inflation, trade policy, and other factors remains, the cumulative evidence from rail traffic points to an economy that is entering the second half of the year with solid momentum.

Rail Traffic Growth Remained Broad-Based in June and the Second Quarter

The breadth of recent gains is becoming increasingly difficult to ignore. Eight of the twenty major carload categories recorded their strongest month of the year in June, while another five posted their second strongest month.

Excluding coal, carloads reached their highest level since August 2018, and sixteen of twenty commodity groups expanded during the second quarter, the broadest quarterly advance since the post-pandemic recovery.

Total second quarter carloads were the highest since late 2019, while intermodal established another monthly record and year-to-date container traffic reached new quarterly and first-half highs.

Intermodal continues to benefit from a favorable combination of factors. Rail service remains strong, trucking has become more expensive, consumer spending continues to support goods movement, and some imports have likely been pulled forward ahead of possible trade policy changes. With the seasonal peak still ahead, intermodal could remain a source of strength during the second half of the year.

The AAR Freight Rail Index climbed to its second-highest level on record, reinforcing the strength in economically sensitive freight.

Manufacturing Is Sending the Same Signal

One of the more encouraging developments this year is that rail traffic and manufacturing data are increasingly telling the same story.

June marked the sixth consecutive month that the ISM Manufacturing PMI® remained above 50%, while manufacturing output reached its highest level in more than three years. New orders also remain near multi-year highs.

Rail volumes are consistent with that picture. Chemical shipments, which are closely tied to manufacturing activity, have now increased from a year earlier for six consecutive months and reached a record during the first half of the year.

Steel related traffic has strengthened as well. Rail shipments of primary metal products posted their second consecutive year over year gain in June, reaching their highest level in nearly five years; recent iron and steel scrap traffic climbed to levels not seen in more than fifteen years.

Other industrial commodities, including petroleum products, lumber, food products, and stone, clay, and glass products, have also posted sustained gains in recent months. Taken together, these trends suggest manufacturing is becoming a more meaningful source of freight demand than it was a year ago.

Not every commodity is participating. Coal continues to reflect longer term changes in energy markets, while motor vehicles and construction-related commodities remain uneven. But those exceptions no longer define the broader picture.

Manufacturing is not the only source of strength. Agriculture continues to perform exceptionally well.

Grain carloads increased 11% in June, marking their twenty seventh gain in the past thirty months. Through the first half of the year, grain volumes were the highest since 1990, supported by strong exports and continued growth in domestic processing. Grain mill products also established new monthly and first half records.

USDA forecasts suggest lower corn and wheat production this year but stronger soybean output. While that could temper grain volumes later this year, exports and domestic processing should continue providing support.

Economic data continue to send mixed signals. Housing remains weak, inflation remains elevated, and policy uncertainty has not disappeared.

A More Complete Picture of the Economy

Economic data continue to send mixed signals. Housing remains weak, inflation remains elevated, and policy uncertainty has not disappeared.

At the same time, manufacturing has strengthened, freight volumes continue to improve, and consumer spending has remained more resilient than many expected. Those are not contradictory observations. They simply remind us that different parts of the economy rarely move in perfect sync.

Taken together, rail and manufacturing indicators suggest the goods-producing sector has regained some of the momentum it lacked over the past several years.

Looking Ahead

No single dataset can determine where the economy is headed. Rail traffic is no exception.

But one lesson from this year is becoming increasingly clear. The recent improvement in freight demand has lasted longer, reached more commodities, and become more consistent than many expected just a few months ago.

Whether that momentum carries through the second half of the year will depend on many factors. For now, however, rail data continue to point to an industrial economy that is expanding on a broader and more durable foundation than it was just a year ago.