RIO is a free monthly publication that provides insights from our economists into what rail traffic says about today’s economy and where the data suggests it could be headed. As part of RIO, the Freight Rail Index (FRI) tracks movement across the most economically sensitive rail traffic commodities. You can find the full report each month on this webpage, with past editions available as PDFs at the bottom of the page. Find past edition PDFs at the bottom of this page.

August 2026 Key Takeaways

- Continued solid rail traffic growth. Total carloads in July rose for the seventh straight month; intermodal was up for the sixth straight month and set a new record for July.

- Broad-based growth. Carload volumes were up in most carload categories again in July, suggesting economic strength extends well beyond a few isolated sectors.

- Manufacturing and rail freight activity are moving together. Manufacturing is expanding at a pace not seen in several years, underscoring the close link between factory output and rail volumes.

- Better than expected just a few months ago. Support for the freight economy has broadened significantly since the start of the year.

U.S. rail traffic in July was much like May and June: broad gains and a positive economic signal.

July extended a pattern that has persisted throughout much of 2026: growth in most rail carload categories and exceptional intermodal volumes.

In July, total U.S. rail carloads rose year over year for the seventh straight month. Through July, total carloads were up 2.7%. Excluding coal, carloads were up 4.3% year to date.

Meanwhile, U.S. rail intermodal volume set a record for July (following a record-setting June) and was up 3.8% year to date. So far this year, rail traffic has grown at a much faster rate than GDP.

Rail traffic growth extended across most categories in July.

Importantly, rail gains in July remained broad-based. Fourteen of the 20 major carload categories posted year-over-year increases, matching June.

This means rail traffic growth is being driven by diverse sources of demand, not just a few key sectors. Whether that’s the result of stronger economic activity, market share gains from other modes, or other factors, strength is widespread across the rail network and is therefore likely to be more durable.

July was the highest-volume or second-highest-volume month of the year for 9 of the 20 major carload categories the AAR tracks — including categories as disparate as nonmetallic minerals, lumber, paper, petroleum products, and steel products — even though the week of July 4th is typically one of the lowest volume weeks of the year for U.S. railroads.

July did not bring good news for every rail commodity.

Most importantly, coal carloads fell in July for the fifth straight month. Coal volumes today are less than half what they were 20 years ago, but coal remains by far the single highest volume rail carload category.

Recent coal volumes reflect continued declines in domestic coal consumption, as well as challenges in coal export markets. With coal, total carloads rose 0.5% in July. Without coal, carloads rose 3.2%.

Notably, rail coal volumes tend to rise or fall for reasons that have little or nothing to do with the state of the economy, so their recent decline does not reflect economic fundamentals.

Grain carloads fluctuate too, for reasons largely unrelated to broader economic conditions. In July, grain carloads were 2.5% above last year, their ninth straight year-over-year gain. July was the first month in 2026 in which grain did not have the biggest absolute year-over-year gain among carload categories. Through the first seven months of 2026, grain carloads were up 13% — nearly 81,000 carloads, more than any other category — thanks mainly to solid grain export growth.

Following up on a record-setting June, U.S. rail intermodal volume in July was the sixth highest for any month on record, even with the July 4th holiday. July 2026 was by far the best July ever for intermodal.

Year-to-date intermodal volume through July this year is a record high.

That’s no accident. It reflects a combination of excellent current rail service levels, higher trucking costs associated with higher diesel prices and fewer available drivers, and continued strong consumer demand for goods.

Together, those factors have put 2026 on pace to be the best year in intermodal history.

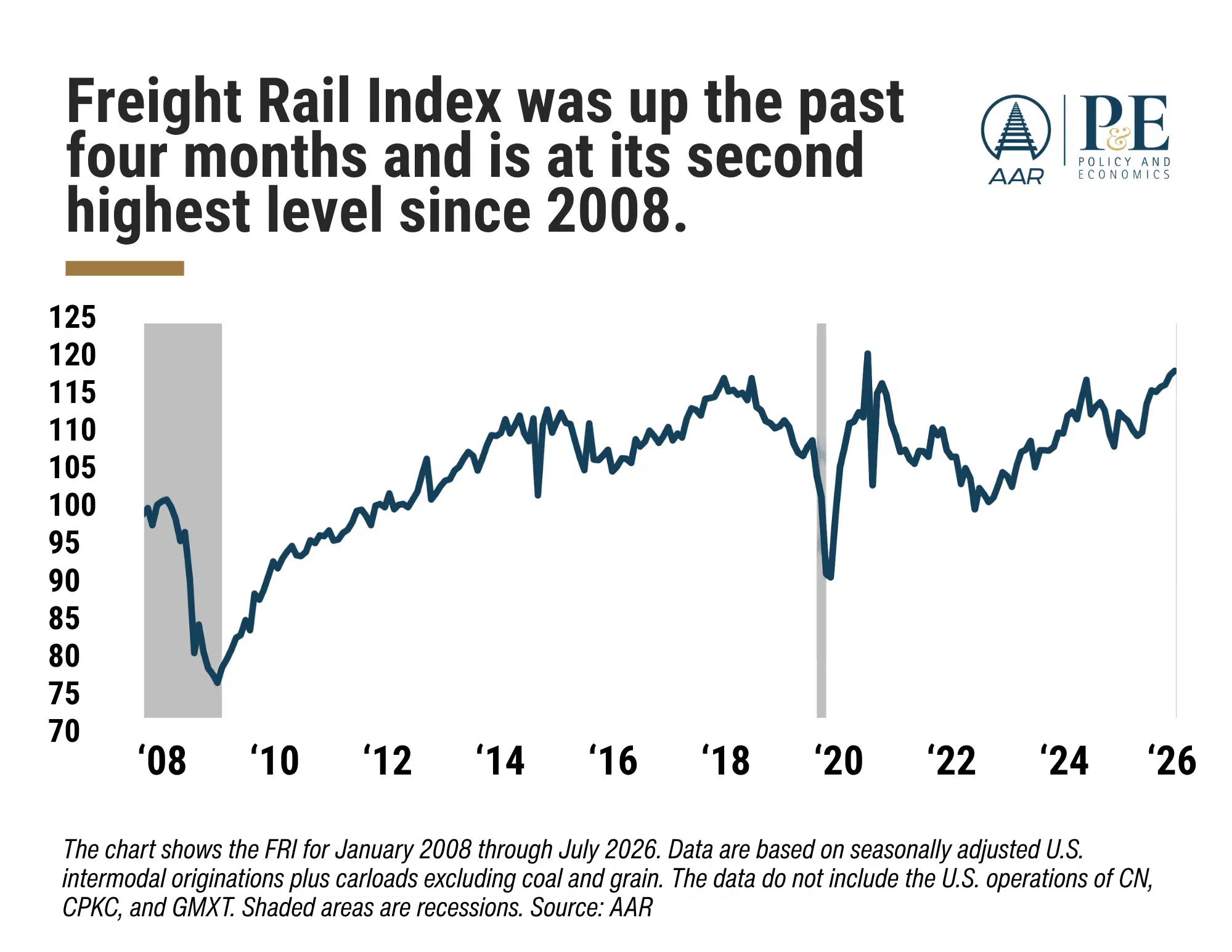

In July, the AAR Freight Rail Index (FRI), which measures seasonally adjusted intermodal and carload volumes excluding coal and grain, rose for the fourth straight month and is now at its second-highest level ever. The FRI’s strength points to continued momentum in goods movement and provides a clear positive signal for near-term economic activity.

Manufacturing momentum continues.

For most of 2023, 2024, and 2025, the U.S. manufacturing sector was sluggish at best. Over this period, the ISM’s Manufacturing PMI® was below 50% nearly every month, implying manufacturing contraction. Manufacturing output was flat or down most months, while manufacturing employment fell steadily.

It’s very different today. The Manufacturing PMI® in July 2026 was 55.7%, its highest level in more than four years and its seventh straight month above 50%. Manufacturing output, which began trending higher in the second half of 2025, has continued those gains through the first half of 2026. Manufacturing employment is higher today than at the end of last year.

That matters to railroads because large swaths of rail traffic are related to manufacturing, whether it’s raw materials, intermediate goods, or final output. Simply put, when manufacturing is healthier, railroads probably are too. Rail volumes in July confirm this point.

Another pertinent metric: rail cars in storage, representing equipment not currently needed to move freight. A decline in stored cars suggests railroads and other freight car owners are putting more equipment back into service, reflecting stronger traffic volumes and more robust demand for rail transportation. Since the beginning of the year, the number of cars in storage has fallen by 53,000 and the share of total cars in storage has fallen from 21.7% to 18.5%.

The broader economy presents a mixed picture.

As is usually the case, recent economic indicators offer a mixed picture.

Some measures are pointing to continued expansion. As noted above, manufacturing has strengthened noticeably in recent months, and the ISM’s services index in July was above 50% (signifying expansion) for the 25th straight month. The unemployment rate fell in July to 4.1%. Consumer spending in June grew at the fastest pace since last August, driving economic growth.

Offsetting these positives, the housing market remains sluggish, inflation is still too high, consumer confidence remains depressed, and uncertainty regarding economic and trade policy persists. July also saw a preliminary loss of 23,000 jobs, the first decline after four months of gains and a sign of softness in the labor market.

The economy seldom moves in lockstep. Even during periods of overall growth, some sectors advance while others struggle. Recent economic data reflect that reality.

Looking Ahead

Rail is not synonymous with the economy, but it’s hard to think of an indicator that provides a clearer read on the nation’s goods-producing and goods-moving sectors. Uncertainty remains a defining feature of the economic outlook, but the pattern emerging from rail traffic in recent months is one of continued expansion, not retrenchment.

The breadth of the gains has been striking. Freight demand has extended beyond a few isolated bright spots to encompass a wide range of commodities, with fewer of the starts and stops that often characterize recoveries. As always, the outlook remains uncertain. But one thing is clear: the freight economy is entering the second half of the year with support from far more industries, more commodities, and more markets than seemed likely at the beginning of the year.